Disability Insurance

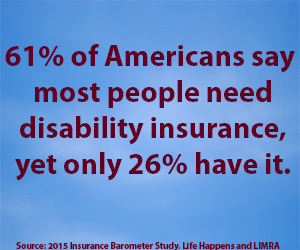

Disability insurance provides you with a source of income when you are unable to work due to a covered injury or illness. What would happen if you were unable to work due to sickness or injury? Could you maintain your current lifestyle without a paycheck for more than a few months?

Disability insurance provides you with a source of income when you are unable to work due to a covered injury or illness. What would happen if you were unable to work due to sickness or injury? Could you maintain your current lifestyle without a paycheck for more than a few months?

Our insurance advisor will work with you and help you decide what options are best for you. We are here to help you protect what matters most.

Disability Insurance: Things to Consider

Listed below are important factors that can affect the type of disability coverage that’s right for you. The best way to make sure that you make a responsible decision is to discuss your specific needs with our insurance professional.

Amount of coverage

While there’s no substitute for a thorough needs analysis conducted by an insurance professional, you’ll find that most policies cover between 50% and 70% of your income. When thinking about how much coverage you need, consider both short-term and long-term expenses, as well as any other sources of disability income, such as investment income or group disability income coverage.

Group disability coverage

Some employers, including most larger ones, offer group disability insurance. However, an employee may still need to consider individual disability insurance because the coverage offered by the company might be insufficient. In this case, the amount of individual insurance you can obtain will be affected by the amount of group coverage you receive.

Elimination period

This is the amount of time you are required to wait after a disability occurs before you can receive benefits. It can vary from as short as 30 days to 90 days or longer. Longer elimination periods generally translate into lower premiums. However, you should be certain that you could afford to meet all of your immediate needs for that period of time if you were to become disabled.

Benefit period

Another policy option concerns the amount of time you will receive benefits. They can last for between one and five years, up to age 65, or even for life, depending on your specific needs. The benefit period will directly impact your premiums, the longer the period, the higher the premium.

Taxable or tax-free income

If your employer pays your insurance premiums, any benefits you receive will be taxable because they are considered income. If you pay your premiums with after-tax dollars, then your benefits will be tax free (according to current IRS regulations).

Retirement

When considering the amount of coverage you need, keep in mind that you will probably want to continue funding your retirement needs, even if you are not working.

Definition of disability

Some plans pay claims if you can no longer perform the duties of your current occupation, while other plans will pay benefits only if you are unable to perform the duties of any occupation. Still others will pay benefits based upon loss of earned income. Each option offers a different level of cost and benefit.

Employers are you looking for group policies? We can help, click here.

Additional Resources:

An Income Protection Guide for Individuals, Families and Business Owners

Calculate your needs

DisabilityCanHappen.org

Whats my PDQ?

This information has been reproduced with the permission of Life Happens, a nonprofit organization dedicated to helping consumers make smart insurance decisions to safeguard their families financial futures. Life Happens does not endorse any insurance company, product or advisor.

© Life Happens 2015. All rights reserved.